What 75% of Reverse Mortgage Servicers Get Wrong About AI Modernization

Executive Summary

Reverse mortgage servicers are increasing investment in AI, yet most are not realizing measurable business value. The issue is not the technology it is the foundation it is built on. Legacy servicing environments remain fragmented, compliance-heavy, and operationally inefficient. Adding AI on top of this complexity often accelerates existing problems instead of solving them. A compliance-first modernization approach aligns data, regulatory requirements, and automation in the right sequence, enabling faster operations, stronger audit readiness, and scalable growth.

Who This Is For

- Heads of Servicing Operations

- Chief Compliance Officers

- CIOs / CTOs in mortgage servicing

- Transformation and risk leaders in BFSI

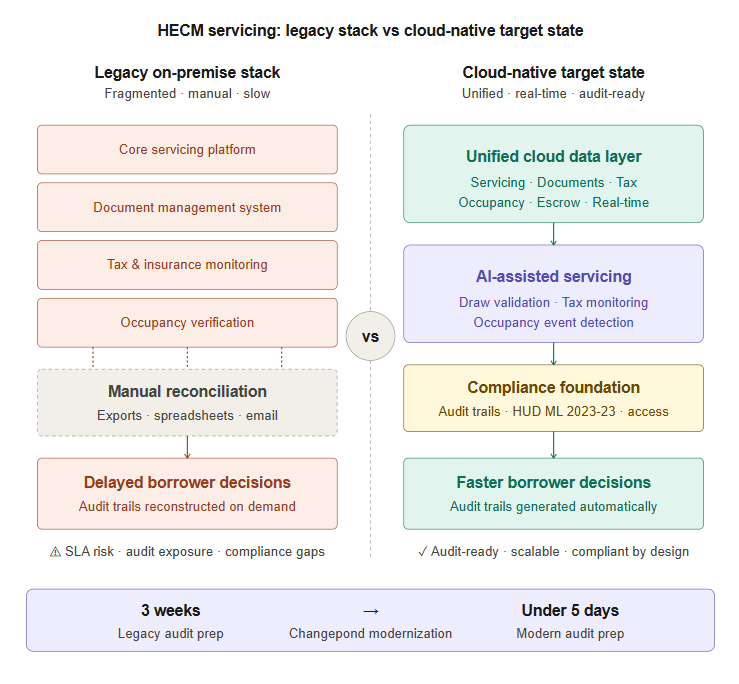

Legacy Servicing Systems Are Increasing Borrower and Compliance Risk

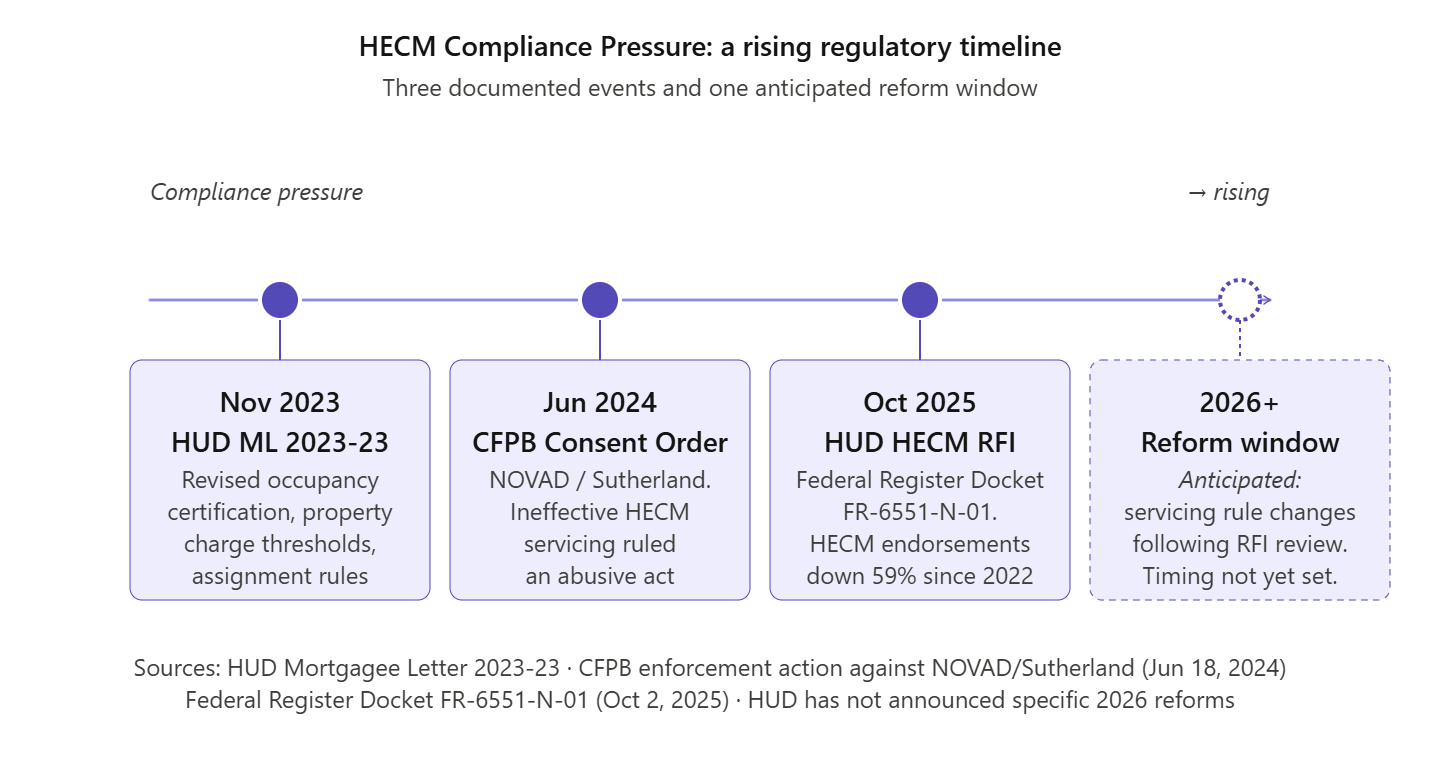

Reverse mortgage servicers are operating under the highest regulatory pressure in over a decade.

- On June 18, 2024, the Consumer Financial Protection Bureau (CFPB) issued a consent order against NOVAD Management Consulting, finding that ineffective HECM servicing constitutes an abusive act under the Consumer Financial Protection Act

- On October 2, 2025, the U.S. Department of Housing and Urban Development (HUD) released its HECM Request for Information (Federal Register Docket FR-6551-N-01), noting HECM endorsements have declined 59% since 2022 and signaling potential changes to servicing rules

Yet most core servicing systems have not fundamentally changed.

A borrower calls about a draw request. The answer exists — but your system cannot access it in real time.

Data is fragmented across servicing platforms, document systems, and tax monitoring tools. Manual reconciliation slows response times, increases errors, and creates compliance blind spots.

According to Stratmor Group (2025), AI adoption among mortgage lenders rose from 15% in 2023 to 38% in 2024. According to FIS and Oxford Economics (2025), cyberthreats, fraud, and operational inefficiencies cost financial services firms an average of $98.5 million annually.

What This Means for The Business:

- Slower borrower response → increased complaint risk

- Higher cost per loan serviced → margin pressure

- Incomplete documentation → audit exposure

- Technology investment → limited ROI

This is not a front-end problem. It is a data and compliance architecture problem.

What a New Borrower Portal Cannot Fix

When core servicing, document management, and tax monitoring operate in silos, no interface upgrade can resolve the delay.

You are accelerating the front door of a building with no corridors.

HUD explicitly acknowledged this operational strain in its October 2, 2025 HECM RFI, linking servicer burden to broader program risk. The National Consumer Law Center (2023) documented borrower harm tied to missed certifications and preventable defaults.

Ryan LaRose, Chief Client and Industry Relations Officer at Celink — which services roughly 75% of the HECM market — has noted that what once required a small team and a basic platform now demands significantly expanded compliance infrastructure and cybersecurity architecture.

Business Impact:

- Missed occupancy certifications → default risk

- Manual workflows → higher servicing cost

- Delayed borrower action → reputational damage

- Weak audit trails → regulatory penalties

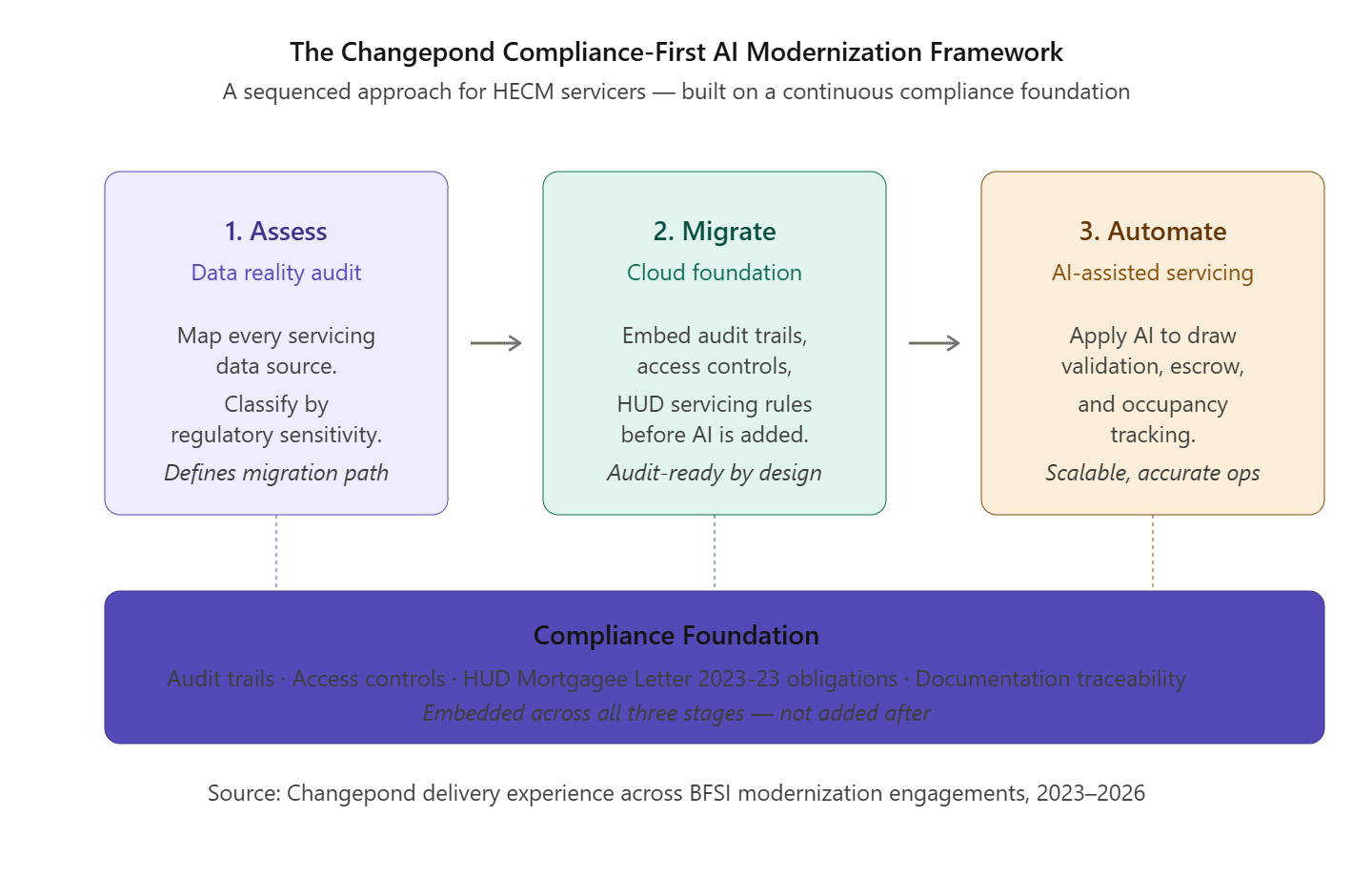

The Changepond Compliance-First AI Modernization Framework

1.Assess : Data Reality Audit

Map all servicing data sources and classify by regulatory sensitivity.

Business value: Early identification of compliance gaps and a clear modernization roadmap.

2.Migrate: Compliance-First Cloud Foundation

Embed audit trails, access controls, and regulatory rules before introducing AI.

Business value: Audit-ready infrastructure from day one and reduced remediation costs.

3.Automate: AI-Assisted Servicing Operations

Apply AI to draw validation, tax monitoring, and occupancy tracking.

Business value: Faster processing, improved decision accuracy, reduced borrower complaints, scalable operations without proportional hiring.

Where Servicers Go Wrong

- Skipping data consolidation → Impact: SLA breaches and operational inefficiency

- Implementing AI before compliance architecture → Impact: Increased audit exposure

- Focusing on low-impact AI use cases → Impact: Limited ROI

- Ignoring parallel-run validation → Impact: Borrower disruption and regulatory escalation

Find Where Your Servicing Stack Is Creating Audit Risk →

What This Looks Like in Practice

A mid-sized US reverse mortgage servicer engaged Changepond to consolidate three legacy on-premise platforms into a unified cloud environment with AI-assisted draw validation and tax monitoring. The migration ran 16 weeks with full parallel-run validation.

Results achieved:

- Draw processing time reduced by 50%

- Audit preparation reduced from 3 weeks to under 5 days

- 30% increase in servicing capacity without additional headcount

| Metric | Legacy State | Modernized State | Business Value |

|---|---|---|---|

| Audit prep | 3–4 weeks | Under 5 days | Significant time savings |

| Draw processing | Manual | 50% faster | Faster borrower decisions |

| Capacity | Fixed by headcount | +30% same team | Deferred hiring cost |

| Occupancy tracking | Manual | Real-time | Lower default risk |

| Documentation | Reconstructed | Always audit-ready | Reduced compliance risk |

“The documentation trail that used to take three weeks to reconstruct now generates automatically. Our last HUD exam took four days of preparation, not four weeks.” —VP Mortgage Operations, Leading Financial Services Company

Changepond Perspective

“Compliance is not a layer you add to a working system. It is the foundation. Get it right and AI multiplies the gain. Skip it and automation accelerates the problem.” — Govindarajan, Financial Services Practice · Changepond Technologies

Key Takeaways

- Regulatory pressure is rising while legacy systems remain static

- AI delivers ROI only when applied to compliance-critical workflows

- Successful modernization follows a clear sequence: Data → Compliance → AI → Validation

The Cost of Waiting

Delaying modernization compounds documentation gaps, operational inefficiencies, and compliance risk. These issues surface at the most critical moments audits, borrower complaints, or regulatory change.

Organizations that modernize with a compliance-first approach build systems where AI delivers sustained, compounding value. Those that delay face significantly higher remediation costs and greater regulatory exposure.

Ready to Modernize - Not Just Evaluate? →

Frequently Asked Questions

What is reverse mortgage servicing modernization?

Migrating HECM servicing from legacy systems to cloud-native infrastructure, then applying AI to high-frequency workflows like draw processing, tax monitoring, and occupancy verification.

How does AI help modernize legacy systems?

Fragmented data across siloed systems, manual compliance workflows that cannot generate the documentation trails HUD now expects, and cybersecurity infrastructure not built for today’s threat environment. The CFPB’s June 2024 consent order and HUD’s October 2025 RFI have both significantly raised the bar.

Where does AI deliver the highest ROI?

In rules-based, high-volume workflows especially draw validation, escrow monitoring, and occupancy tracking.

How do you modernize without disrupting borrowers?

Through phased migration with parallel-run validation and predefined rollback criteria before go-live.

What is changing from a regulatory perspective?

HUD and CFPB expectations are increasing around documentation, borrower communication, and compliance traceability requiring systems that are audit-ready by design.